Covariates#

Sections about past and future covariates were written for darts version 0.15.0 and later. Sections about static covariates were written for darts version 0.20.0 and later.

Summary - TL;DR#

In Darts, covariates refer to external data that can be used as inputs to models to help improve forecasts. In the context of forecasting models, the target is the series to be forecasted/predicted, and the covariates themselves are not predicted. We distinguish three kinds of covariates:

past covariates are (by definition) covariates known only into the past (e.g. measurements)

future covariates are (by definition) covariates known into the future (e.g., weather forecasts)

static covariates are (by definition) covariates constant over time (e.g., product IDs). Check out our static covariates example notebook here for more information.

Models in Darts accept past_covariates and/or future_covariates in their fit() and predict() methods, depending on their capabilities (some models accept no covariates at all). Both target and covariates must be a TimeSeries object. The models will raise an error if covariates were used that are not supported.

# create one of Darts' forecasting models

model = SomeForecastingModel(...)

# fitting model with past and future covariates

model.fit(target=target,

past_covariates=past_covariates_train,

future_covariates=future_covariates_train)

# predict the next n=12 steps

model.predict(n=12,

series=target, # only required for Global Forecasting Models

past_covariates=past_covariates_pred,

future_covariates=future_covariates_pred)

Different to past and future covariates, static covariates must be embedded in the target series. Because of that, working with static covariates follows a different methodology. You can check out how to use static covariates in this example.

If you have several covariate variables that you want to use as past (or future) covariates, you have to stack() all of them into a single past_covariates (or future_covariates) object.

# stack two TimeSeries with stack()

past_covariates = past_covariates.stack(other_past_covariates)

# or with concatenate()

from darts import concatenate

past_covariates = concatenate([past_covariates, other_past_covariates], axis=1)

Darts’ forecasting models expect one past and/or future covariate series per target series. If you use multiple target series with one of Darts’ Global Forecasting Models, you must supply the same number of dedicated covariates to fit().

# fit using multiple (two) target series

model.fit(target=[target, target_2],

past_covariates=[past_covariates, past_covariates_2],

# optional future_covariates,

)

# you must give the specific target and covariate series that you want to predict

model.predict(n=12,

series=target_2,

past_covariates=past_covariates_2,

# optional future_covariates,

)

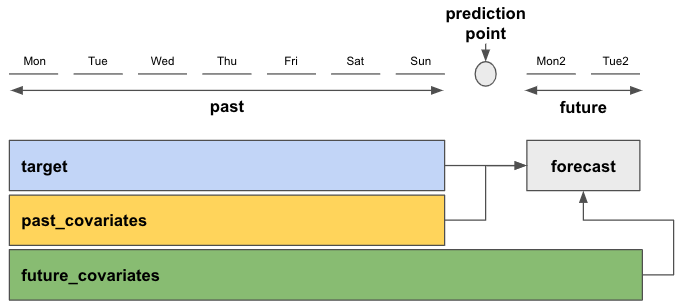

If you train a model using past_covariates, you’ll have to provide these past_covariates also at prediction time to predict(). This applies to future_covariates too, with a nuance that future_covariates have to extend far enough into the future at prediction time (all the way to the forecast horizon n). This can be seen in the graph below. past_covariates needs to include at least the same time steps as target, and future_covariates must include at least the same time span plus additional n forecast horizon time steps.

You can use the same *_covariates for both training and prediction, given that they contain the required time spans.

Figure 1: Top level summary of how forecasting models work with target and covariates for a prediction with forecast horizon n=2

There are some extra nuances that might be good to know. For instance, deep learning models in Darts

can (in general) forecast output_chunk_length points at a time. However it is still possible for models

trained with past covariates to make forecasts for some horizon n > output_chunk_length if the past_covariates

are known far enough into the future. In such cases, the forecasts are obtained by consuming future values

of the past covariates, and using auto-regression on the target series. If you want to know more details, read on.

Introduction - What are covariates (in Darts)?#

Past, future and static covariates provide additional information/context that can be useful to improve the prediction of the target series. The target series is the variable we wish to predict the future for. We do not predict the covariates themselves, only use them for prediction of the target.

Past and future covariates hold information about the past (up to and including present time) or future. This is always relative to the prediction point (in time) after which we want to forecast the future.

In Darts, we refer to these two types as past_covariates and future_covariates.

Static covariates hold time independent (constant / static) information about the target series. We refer to them as static_covariates. They must be embedded in the target series. Working with static covariates follows a slightly different approach than with past or future covariates. Check out our notebook on static covariates to learn more.

Darts’ forecasting models have different support modes for *_covariates. Some do not support covariates at all, others support only past or future covariates and some even support all three (more on that in this subsection).

Let’s have a look at some examples of past, future, and static covariates:

past_covariates: typically measurements (past data) or temporal attributesdaily average measured temperatures (known only in the past)

day of week, month, year, …

future_covariates: typically forecasts (future known data) or temporal attributesdaily average forecasted temperatures (known in the future)

day of week, month, year, …

static_covariates: time independent/constant/statictargetcharacteristicscategorical:

location of

target(country, city, .. name)targetidentifier: (product ID, store ID, …)

numerical:

population of

target’s country/market area (assuming it stays constant over the forecasting horizon)average temperature of

target’s region (assuming it stays constant over the forecasting horizon)

Temporal attributes are powerful because they are known in advance and can help models capture trends and / or seasonal patterns of the target series.

Static attributes are powerful when working with multiple targets (either multiple TimeSeries, or multivariate series containing multiple dimensions each). The time independent information can help models identify the nature/environment of the underlying series and improve forecasts across different targets.

In this guide we’ll focus on past and future covariates. Here’s a simple rule-of-thumb to know if your series are past or future covariates:

If the values are known in advance, they are future covariates (or can be used as past covariates). If they are not, they must be past covariates.

You might imagine cases where you want to train a model supporting only past_covariates (such as TCNModel, see Table 1). In this case, you could use for instance say, the forecasted temperature as a past covariate for the model even though you also have access to temperature forecasts in the future. Knowing such “future values of past covariates” can allow you to make forecasts further into the future (for Darts’ deep learning models with forecast horizons n > output_chunk_length). Similarly most models consuming future covariates can also use “historic values of future covariates”.

Side note: if you don’t have future values (e.g. of measured temperatures), nothing prevents you from applying one of Darts’ forecasting models to forecast future temperatures, and then use this as future_covariates. Darts is not attempting to forecast the covariates for you, as this would introduce an extra “hidden” modeling step, which we think is best left to the users.

Forecasting Model Covariate Support#

Darts’ forecasting models accept optional past_covariates and / or future_covariates in their fit() and predict() methods (and static_covariates embedded in the target series), depending on their capabilities. Table 1 shows the supported covariate types for each model. The models will raise an error if covariates were used that are not supported.

Local Forecasting Models (LFMs):#

LFMs are models that can be trained on a single target series only. In Darts most models in this category tend to be simpler statistical models (such as ETS or ARIMA). LFMs accept only a single target (and covariate) time series and usually train on the entire series you supplied when calling fit() at once. They can also predict in one go for any number of predictions n after the end of the training series.

Global Forecasting Models (GFMs)#

GFMs are models that can be trained on multiple target (and covariate) time series. Different to LFMs, the GFMs train and predict on fixed-length sub-samples (chunks) of the input data. In Darts, these are the global (naive) baseline models, regression models, PyTorch (Lightning)-based models (neural networks), foundation models, as well ensemble models (depending on their ensemble model and / or the forecasting models they ensemble).

Model |

Past Covariates |

Future Covariates |

Static Covariates |

|---|---|---|---|

Local Forecasting Models (LFMs) |

|||

Naive Baselines (a) |

|||

✅ |

|||

✅ |

|||

✅ |

|||

✅ |

|||

FFT (Fast Fourier Transform) |

|||

✅ |

|||

Croston method |

✅ |

||

✅ |

|||

✅ |

|||

✅ |

|||

✅ |

|||

✅ |

|||

✅ |

|||

✅ |

|||

Global Forecasting Models (GFMs) |

|||

Global Naive Baselines (b) |

|||

SKLearn-Like Regression Models (c) |

✅ |

✅ |

✅ |

SKLearn-Like Classification Models (d) |

✅ |

✅ |

✅ |

RNNModel (e) |

✅ |

||

BlockRNNModel (f) |

✅ |

✅ |

✅ |

✅ |

|||

✅ |

|||

✅ |

|||

✅ |

|||

✅ |

✅ |

✅ |

|

✅ |

✅ |

✅ |

|

✅ |

✅ |

✅ |

|

✅ |

✅ |

✅ |

|

✅ |

✅ |

✅ |

|

✅ |

✅ |

✅ |

|

✅ |

✅ |

||

Ensemble Models (h) |

✅ |

✅ |

✅ |

Conformal Prediction Models (i) |

✅ |

✅ |

✅ |

Table 1: Darts’ forecasting models and their covariate support

(a) Naive Baselines including NaiveDrift, NaiveMean, NaiveMovingAverage, and NaiveSeasonal.

(b) Global Naive Baselines including GlobalNaiveAggregate, GlobalNaiveDrift, and GlobalNaiveSeasonal.

(c) SKLearn-Like Regression Models including SKLearnModel, LinearRegressionModel, RandomForestModel, LightGBMModel, XGBModel, and CatBoostModel. SKLearnModel is a special kind of GFM which can use arbitrary lags on covariates (past and/or future) and past targets to predict continuous numerical values.

(d) SKLearn-Like Classification Models including SKLearnClassifierModel, LightGBMClassifierModel, XGBClassifierModel, and CatBoostClassifierModel. SKLearnClassifierModel is a special kind of GFM which can use arbitrary lags on covariates (past and/or future) and past targets to predict categorical class labels.

(e) RNNModel including LSTM and GRU; equivalent to DeepAR in its probabilistic version

(f) BlockRNNModel including LSTM and GRU

(g) NeuralForecastModel covariate support depends on the NeuralForecast base model used. See NeuralForecast model catalog for more details.

(h) Ensemble Model including RegressionEnsembleModel, and NaiveEnsembleModel. The covariate support is given by the covariate support of the ensembled forecasting models.

(i) Conformal Prediction Model including ConformalNaiveModel, and ConformalQRModel. The covariate support is given by the covariate support of the underlying forecasting model.

Quick guide on how to use past and/or future covariates with Darts’ forecasting models#

It is very simple to use covariates with Darts’ forecasting models. There are just some requirements they have to fulfill.

Just like the target series, each of your past and / or future covariates series must be a TimeSeries object. When you train your model with fit() using past and /or future covariates, you have to supply the same types of covariates to predict(). Depending on the choice of your model and how long your forecast horizon n is, there might be different time span requirements for your covariates. You can find these requirements in the next subsection.

You can even use the same *_covariates for fitting and prediction if they contain the required time spans. This is because Darts will “intelligently” slice them for you based on the target time axis.

# create one of Darts' forecasting model

model = SomeForecastingModel(...)

# fit the model

model.fit(target,

past_covariates=past_covariate,

future_covariates=future_covariates)

# make a prediction with the same covariate types

pred = model.predict(n=1,

series=target, # this is only required for GFMs

past_covariates=past_covariates,

future_covariates=future_covariates)

To use multiple past and / or future covariates with your target, you have to stack them all together into a single dedicated TimeSeries:

# stack() time series

past_covariates = past_covariates.stack(past_covariates2)

# or concatenate()

from darts import concatenate

past_covariates = concatenate([past_covariates, past_covariates2, ...], axis=1)

GFMs can be trained on multiple target series. You have to supply one covariate TimeSeries per target TimeSeries you use with fit(). At prediction time you have to specify which target series you want to predict and supply the corresponding covariates:

from darts.models import NBEATSModel

# multiple time series

all_targets = [target1, target2, ...]

all_past_covariates = [past_covariates1, past_covariates2, ...]

# create a GFM model, train and predict

model = NBEATSModel(input_chunk_length=1, output_chunk_length=1)

model.fit(all_targets,

past_covariates=all_past_covariates)

pred = model.predict(n=1,

series=all_targets[0],

past_covariates=all_past_covariates[0])

Covariate time span requirements for Local and Global Forecasting Models#

There are differences in how Darts’ “Local” and “Global” Forecasting Models perform training and prediction. Specifically, how they extract/work with the data supplied during fit() and predict().

Depending on the model you use and how long your forecast horizon n is, there might be different time span requirements for your covariates.

Local Forecasting Models (LFMs):#

LFMs usually train on the entire target and future_covariates series (if supported) you supplied when calling fit() at once. They can also predict in one go for forecast horizon n after the end of the target.

Time span requirements to use the same future covariates series for both fit() and predict():

future_covariates: at least the same time span astargetplus the nextntime steps after the end oftarget

Global Forecasting Models (GFMs):#

GFMs train and predict on fixed-length chunks (sub-samples) of the target and *_covariates series (if supported). Each chunk contains an input chunk - representing the sample’s past - and an output chunk - the sample’s future. The length of these chunks has to be specified at model creation with parameters input_chunk_length and output_chunk_length (one notable exception is RNNModel which always uses an output_chunk_length of 1).

Depending on your forecast horizon n, the model can either predict in one go, or auto-regressively, by predicting on multiple chunks in the future. That is the reason why when predicting with past_covariates you have to supply additional “future values of your past_covariates”.

Time span requirements to use the same past and / or future covariates series for both fit() and predict():

with

n <= output_chunk_length:past_covariates: at least the same time span astargetfuture_covariates: at least the same time span astargetplus the nextoutput_chunk_lengthtime steps after the end oftarget

with

n > output_chunk_length:past_covariates: at least the same time span astargetplus the nextn - output_chunk_lengthtime steps after the end oftargetfuture_covariates: at least the same time span astargetplus the nextntime steps after the end oftarget

If you want to know more details about how covariates are used behind the scenes in Global Forecasting Models, read our guide on Torch Forecasting Models (PyTorch based GFMs). It gives a step-by-step explanation of the training and prediction process using one of our Torch Forecasting Models.

Examples#

Here are a few examples showcasing how to use covariates with Darts forecasting models: