Anomaly Detection Darts Module#

This notebook showcases some of the functionalities of Darts’ Anomaly Detection Module. We’ll look at Anomaly Scorers, Detectors, Aggregators and Anomaly Models.

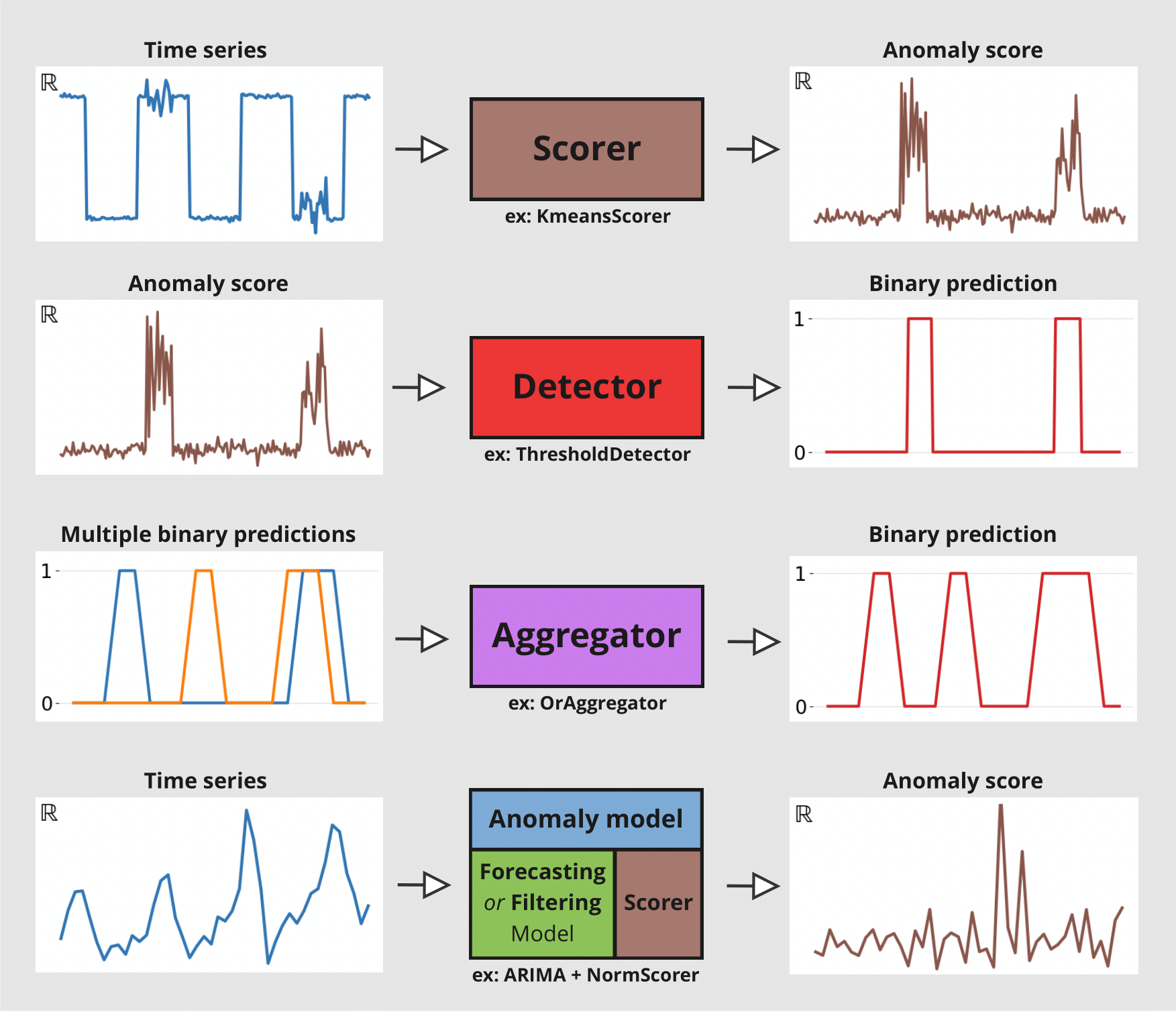

Scorers: compute anomaly scores time series, either only on the target series or between the target series and a forecasted/predicted series. They are the core of the anomaly detection module.Detectors: transform time series (such as anomaly scores) into binary anomaly time series. The presence of an anomaly is flagged with1, and0otherwise.Aggregators: reduce a multivariate binary time series (e.g., where each component represents the anomaly score of a different series component/model) into a univariate binary time series.Anomaly Models: offer a convenient way to produce anomaly scores from any of Darts’ global forecasting models or filtering models by comparing the models’ predictions with actual observations. Each Anomaly Model takes one forecasting/filtering model and one or multiple scorers. The model produces some predictions, which are fed together with the actual series to the scorer(s). It will return anomaly scores for each scorer.

The figure below illustrates the different input/output for each tool:

The notebook is devided into two sections:

How to use

ForecastingAnomalyModelto find anomalies in the number of taxi passengers in New York.How to use an

AnomalyScorerand the importance of its windowing capabilities on two toy datasets.

First, some necessary imports:

[1]:

# fix python path if working locally

from utils import fix_pythonpath_if_working_locally

fix_pythonpath_if_working_locally()

%matplotlib inline

[2]:

%load_ext autoreload

%autoreload 2

%matplotlib inline

[ ]:

# use darts plotting style

from darts import set_option

set_option("plotting.use_darts_style", True)

[3]:

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

from darts import TimeSeries

from darts.ad import (

ForecastingAnomalyModel,

KMeansScorer,

NormScorer,

WassersteinScorer,

)

from darts.ad.utils import (

eval_metric_from_scores,

show_anomalies_from_scores,

)

from darts.dataprocessing.transformers import Scaler

from darts.datasets import TaxiNewYorkDataset

from darts.metrics import mae, rmse

from darts.models import SKLearnModel

/Users/dennisbader/miniconda3/envs/darts310_test/lib/python3.10/site-packages/statsforecast/utils.py:237: FutureWarning: 'M' is deprecated and will be removed in a future version, please use 'ME' instead.

"ds": pd.date_range(start="1949-01-01", periods=len(AirPassengers), freq="M"),

Anomaly Model: Taxi passengers in NY#

Load and visualize the data#

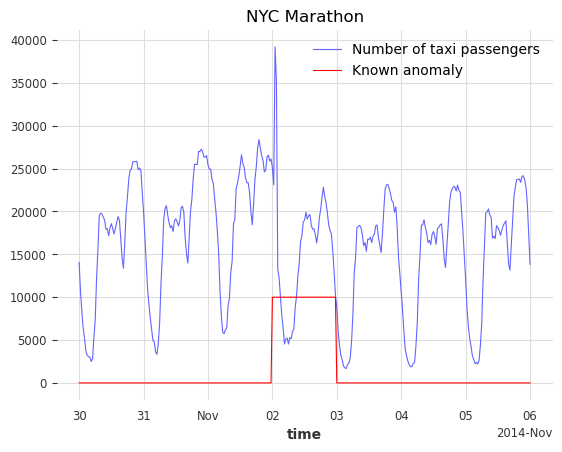

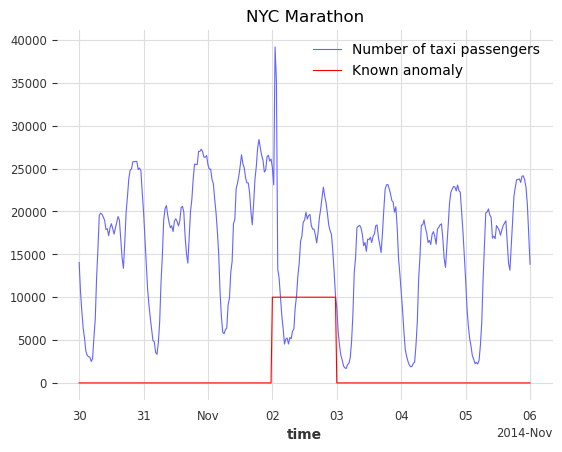

Information on the data:

Univariate Time Series (represents the number of taxi passengers in New York)

During a period of 8 months (2014-07 to 2015-01)

Frequency of 30 minutes

In this example, anomalies are subjective. It can be defined as periods where the demand for taxis is abnormal (different than what should be expected). Based on this definition, the following five dates can be considered anomalies:

NYC Marathon - 2014-11-02

Thanksgiving - 2014-11-27

Christmas - 2014-12-24/25

New Years - 2015-01-01

Snow Blizzard - 2015-01-26/27

[4]:

# load the data

series_taxi = TaxiNewYorkDataset().load()

# define start and end dates for some known anomalies

anomalies_day = {

"NYC Marathon": ("2014-11-02 00:00", "2014-11-02 23:30"),

"Thanksgiving ": ("2014-11-27 00:00", "2014-11-27 23:30"),

"Christmas": ("2014-12-24 00:00", "2014-12-25 23:30"),

"New Years": ("2014-12-31 00:00", "2015-01-01 23:30"),

"Snow Blizzard": ("2015-01-26 00:00", "2015-01-27 23:30"),

}

anomalies_day = {

k: (pd.Timestamp(v[0]), pd.Timestamp(v[1])) for k, v in anomalies_day.items()

}

# create a series with the binary anomaly flags

anomalies = pd.Series([0] * len(series_taxi), index=series_taxi.time_index)

for start, end in anomalies_day.values():

anomalies.loc[(start <= anomalies.index) & (anomalies.index <= end)] = 1.0

series_taxi_anomalies = TimeSeries.from_series(anomalies)

# plot the data and the anomalies

fig, ax = plt.subplots(figsize=(15, 5))

series_taxi.plot(label="Number of taxi passengers", linewidth=1, color="#6464ff")

(series_taxi_anomalies * 10000).plot(label="5 known anomalies", color="r", linewidth=1)

plt.show()

[5]:

def plot_anom(selected_anomaly, delta_plotted_days):

one_day = series_taxi.freq * 24 * 2

anomaly_date = anomalies_day[selected_anomaly][0]

start_timestamp = anomaly_date - delta_plotted_days * one_day

end_timestamp = anomaly_date + (delta_plotted_days + 1) * one_day

series_taxi[start_timestamp:end_timestamp].plot(

label="Number of taxi passengers", color="#6464ff", linewidth=0.8

)

(series_taxi_anomalies[start_timestamp:end_timestamp] * 10000).plot(

label="Known anomaly", color="r", linewidth=0.8

)

plt.title(selected_anomaly)

plt.show()

for anom_name in anomalies_day:

plot_anom(anom_name, 3)

break # remove this to see all anomalies

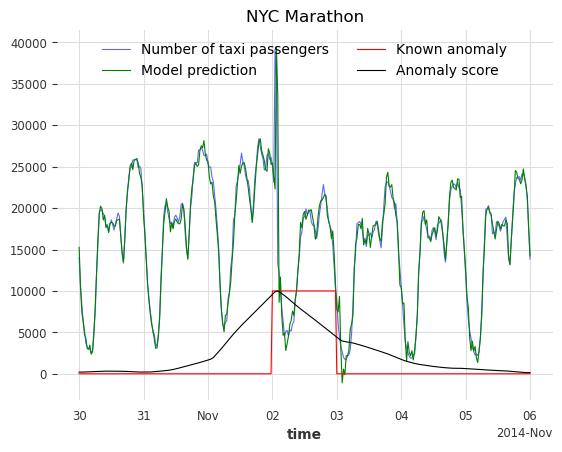

The goal would be to detect these five irregular periods and identify other possible abnormal days.

Train a Darts forecasting model#

We will use a SKLearnModel to predict the number of taxi passengers. The first 4500 timestamps will be used to train the model. The training set is considered to be anomaly-free, the five considered anomalies are located after the 4500th timestamps. The number of lags is set to 1 week, assuming the demand follows a periodicity of 1 week. To help the model, additional information on the targeted series is passed as covariates (the hour and the day of the week).

[6]:

# split the data in a training and testing set

s_taxi_train = series_taxi[:4500]

s_taxi_test = series_taxi[4500:]

# Add covariates (hour and day of the week)

add_encoders = {

"cyclic": {"future": ["hour", "dayofweek"]},

}

# one week corresponds to (7 days * 24 hours * 2) of 30 minutes

one_week = 7 * 24 * 2

forecasting_model = SKLearnModel(

lags=one_week,

lags_future_covariates=[0],

output_chunk_length=1,

add_encoders=add_encoders,

)

forecasting_model.fit(s_taxi_train)

[6]:

SKLearnModel(lags=336, lags_past_covariates=None, lags_future_covariates=[0], output_chunk_length=1, output_chunk_shift=0, add_encoders={'cyclic': {'future': ['hour', 'dayofweek']}}, model=None, multi_models=True, use_static_covariates=True)

Use a Forecasting Anomaly Model#

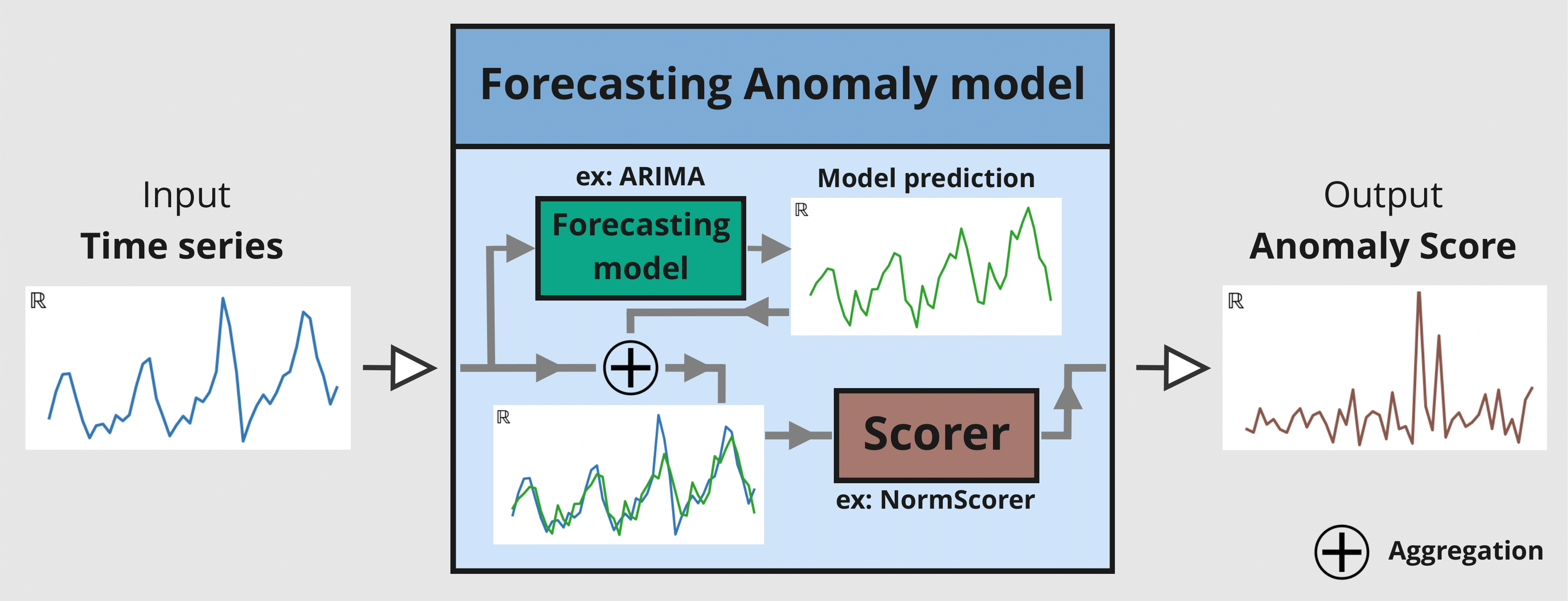

The anomaly model consists of two inputs:

a fitted

GlobalForecastingModel(you can find a list here. If the model hasn’t been fitted, set parameterallow_model_trainingtoTruewhen callingfit())a single or list of

AnomalyScorer(trainable or not)

For this example, three scorers will be used:

NormScorer(window is by default set to 1)WassersteinScorerwith a half-day window (24 timestamps) and no window aggregationWassersteinScorerwith a full-day window (48 timestamps) including window aggregation

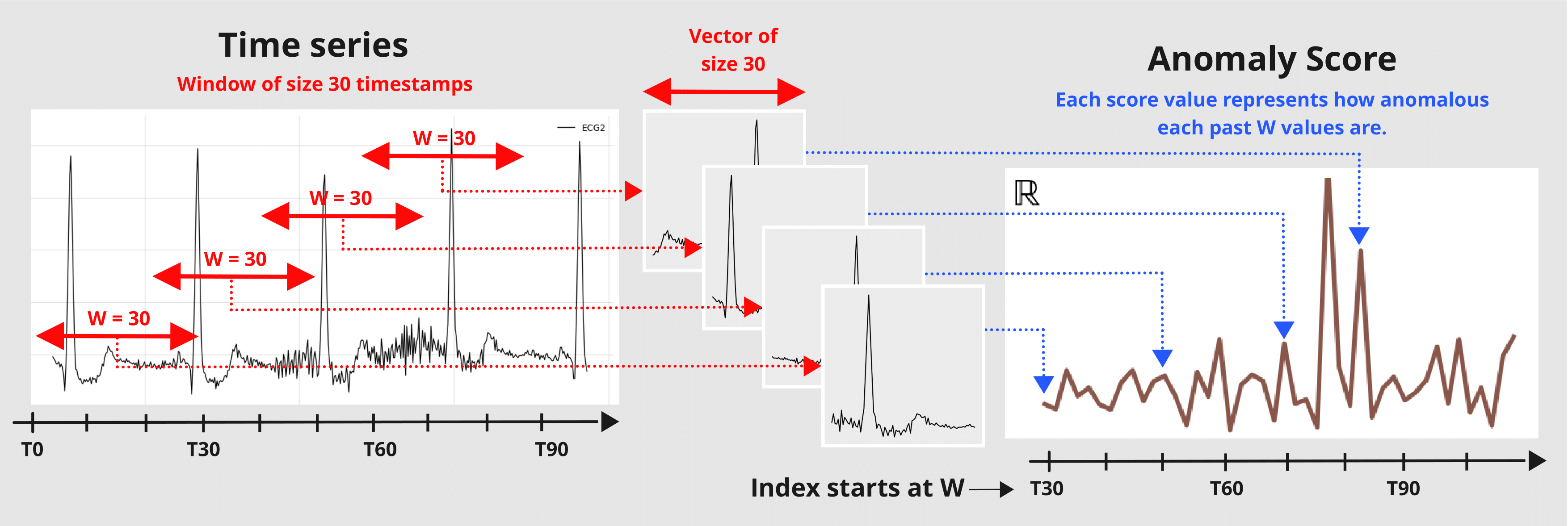

The window parameter is an integer value indicating the window size used by the scorer to transform the series into an anomaly score. A scorer will slice the given series into subsequences of size W and returns a value indicating how anomalous these subset of W values are.

The window_agg can be used to transform the window-wise scores into point-wise scores by aggregating all anomaly scores from each window that the point was included in.

The following figure illustrates the mechanism of a Forecasting Anomaly model:

Using the main functions: fit(), score(), eval_metric() and show_anomalies()#

[7]:

# with timestamps of 30 minutes

half_a_day = 2 * 12

full_day = 2 * 24

# instantiate the anomaly model with: one fitted model, and 3 scorers

anomaly_model = ForecastingAnomalyModel(

model=forecasting_model,

scorer=[

NormScorer(ord=1),

WassersteinScorer(window=half_a_day, window_agg=False),

WassersteinScorer(window=full_day, window_agg=True),

],

)

Now let’s train the anomaly model with fit(). In sequence it will:

fit the forecasting model on the given series if it has not been fitted yet and

allow_model_training=True.generate historical forecasts for the given series.

feed the historical forecasts to each fittable/trainable scorer:

compute the differences between the forecasts and the given series (controled by the scorers

diff_fn, see Darts “per time step” metrics here)train the scorer on these differences

You can control how the historical forecasts are generated when calling fit() (the supported parameters are here).

[8]:

START = 0.1

anomaly_model.fit(s_taxi_train, start=START, allow_model_training=False, verbose=True)

[8]:

<darts.ad.anomaly_model.forecasting_am.ForecastingAnomalyModel at 0x2905d0130>

We call the function score() to compute the anomaly scores of a new series s_taxi_test. It returns the scores from each scorer in the anomaly model. We will use the results in the next section. With return_model_prediction=True, we can additionally get the historical forecasts generated by the forecasting model.

[9]:

anomaly_scores, model_forecasting = anomaly_model.score(

s_taxi_test, start=START, return_model_prediction=True, verbose=True

)

pred_start = model_forecasting.start_time()

[10]:

# compute the MAE and RMSE on the test set

print(

f"On testing set -> MAE: {mae(model_forecasting, s_taxi_test)}, RMSE: {rmse(model_forecasting, s_taxi_test)}"

)

# plot the data and the anomalies

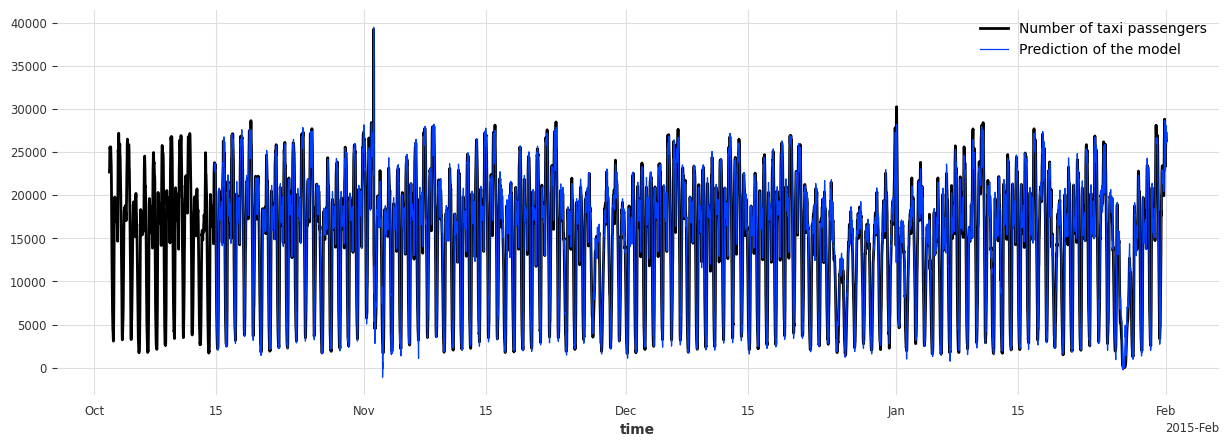

fig, ax = plt.subplots(figsize=(15, 5))

s_taxi_test.plot(label="Number of taxi passengers")

model_forecasting.plot(label="Prediction of the model", linewidth=0.9)

plt.show()

On testing set -> MAE: 595.190366262045, RMSE: 896.6287614972252

To evaluate the anomaly model, we call the function eval_metric(). It outputs the score of an agnostic threshold metric (“AUC-ROC” or “AUC-PR”), between the predicted anomaly score time series and some known binary ground-truth time series indicating the presence of actual anomalies.

It will return a dictionary containing the name of the scorer and its score.

[11]:

metric_names = ["AUC_ROC", "AUC_PR"]

metric_data = []

for metric_name in metric_names:

metric_data.append(

anomaly_model.eval_metric(

anomalies=series_taxi_anomalies,

series=s_taxi_test,

start=START,

metric=metric_name,

)

)

pd.DataFrame(data=metric_data, index=metric_names).T

[11]:

| AUC_ROC | AUC_PR | |

|---|---|---|

| Norm (ord=1)_w=1 | 0.658074 | 0.215601 |

| WassersteinScorer_w=24 | 0.884915 | 0.609469 |

| WassersteinScorer_w=48 | 0.950035 | 0.687788 |

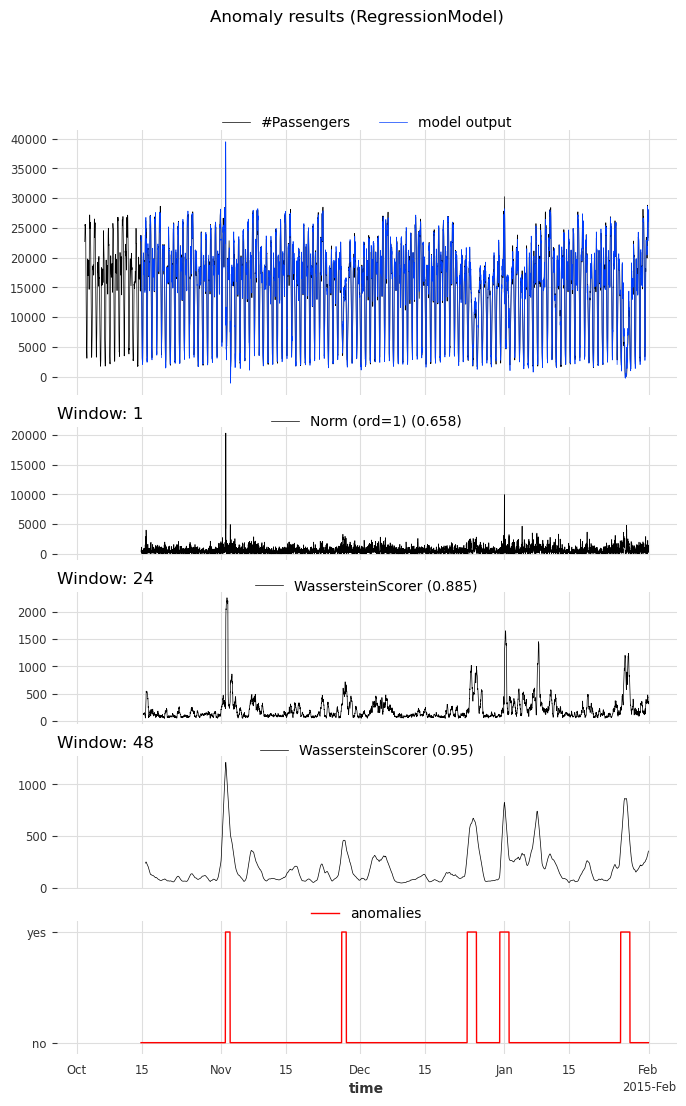

We can see that the anomaly model, using the WassersteinScorer, can separate the abnormal days from the normal ones. The AUC ROC is above 0.9. Additionally, a window of size 48 timestamps (24 hours) is a better option than a window of size 24 timestamps (12 hours).

We call the function show_anomalies() to visualize the results. It plots the forecasts, predicted scores, the input series, and the actual anomalies (if provided). The scorers with different windows will be separated. It is possible to compute a metric that will be shown next to the scorer’s name.

[12]:

anomaly_model.show_anomalies(

series=s_taxi_test,

anomalies=series_taxi_anomalies[pred_start:],

start=START,

metric="AUC_ROC",

)

Convert an anomaly score to a binary prediction with a Detector#

Darts’ Anomaly Detectors convert anomaly scores into binary anomlies/predictions. In this example, we’ll use the QuantileDetector.

It detects anomalies based on the quantile values (high_quantile and/or low_quantile) of historical data. It flags times as anomalous when the values exceed these quantile thresholds. In this example, the anomaly scores were computed for the absolute residuals of the model. It is lower-bound by 0. We set low_quantile=None (default), as we only want to flag values above high_quantile.

We set high_quantile to 0.95. This value must be chosen carefully, as it will convert the (1- high_quantile) * 100 % biggest anomaly scores into a prediction of anomalies. In our case, we want to see the 5% most anomalous timestamps.

Note: You can also use

ThresholdDetectorto define some fixed value thresholds for anomaly detection

[13]:

from darts.ad.detectors import QuantileDetector

contamination = 0.95

detector = QuantileDetector(high_quantile=contamination)

[14]:

# use the anomaly score that gave the best AUC ROC score: Wasserstein anomaly score with a window of 'full_day'

best_anomaly_score = anomaly_scores[-1]

# fit and detect on the anomaly scores, it will return a binary prediction

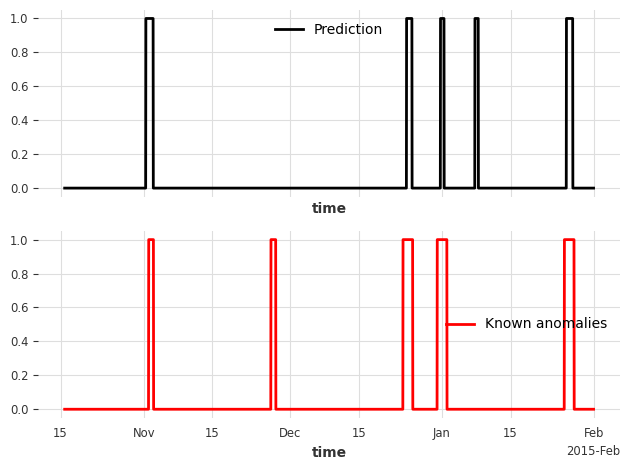

anomaly_pred = detector.fit_detect(series=best_anomaly_score)

# plot the binary prediction

fig, (ax1, ax2) = plt.subplots(nrows=2, sharex=True)

anomaly_pred.plot(label="Prediction", ax=ax1)

series_taxi_anomalies[anomaly_pred.start_time() :].plot(

label="Known anomalies", ax=ax2, color="red"

)

fig.tight_layout()

[15]:

for metric_name in ["accuracy", "precision", "recall", "f1"]:

metric_val = detector.eval_metric(

pred_scores=best_anomaly_score,

anomalies=series_taxi_anomalies,

window=full_day,

metric=metric_name,

)

print(metric_name + f": {metric_val:.2f}/1")

accuracy: 0.91/1

precision: 0.76/1

recall: 0.32/1

f1: 0.45/1

Using the functions show_anomalies_from_scores(), eval_metric_from_scores()#

Internally, methods eval_metric() and show_anomalies() call eval_metric_from_scores() and show_anomalies_from_scores(), respectively. We can also call them directly with pre-computed anomaly scores to avoid having to re-generate the scores each time.

Let’s reproduce the results from above. Both functions require the window sizes used to compute each of the anomaly scores. In our case, the window sizes were 1, 24 (half_a_day), 48 (full_day).

[16]:

windows = [1, half_a_day, full_day]

scorer_names = [f"{scorer}_{w}" for scorer, w in zip(anomaly_model.scorers, windows)]

metric_data = {"AUC_ROC": [], "AUC_PR": []}

for metric_name in metric_data:

metric_data[metric_name] = eval_metric_from_scores(

anomalies=series_taxi_anomalies,

pred_scores=anomaly_scores,

window=windows,

metric=metric_name,

)

pd.DataFrame(index=scorer_names, data=metric_data)

[16]:

| AUC_ROC | AUC_PR | |

|---|---|---|

| Norm (ord=1)_1 | 0.658074 | 0.215601 |

| WassersteinScorer_24 | 0.884915 | 0.609469 |

| WassersteinScorer_48 | 0.950035 | 0.687788 |

As expected, the AUC ROC and AUC PR values are identical to before.

For visualizing the anomalies:

if we want to compute a metric, we need to specify the window sizes as well

optionally, we can indicate the scorers’ names that generated the scores

[17]:

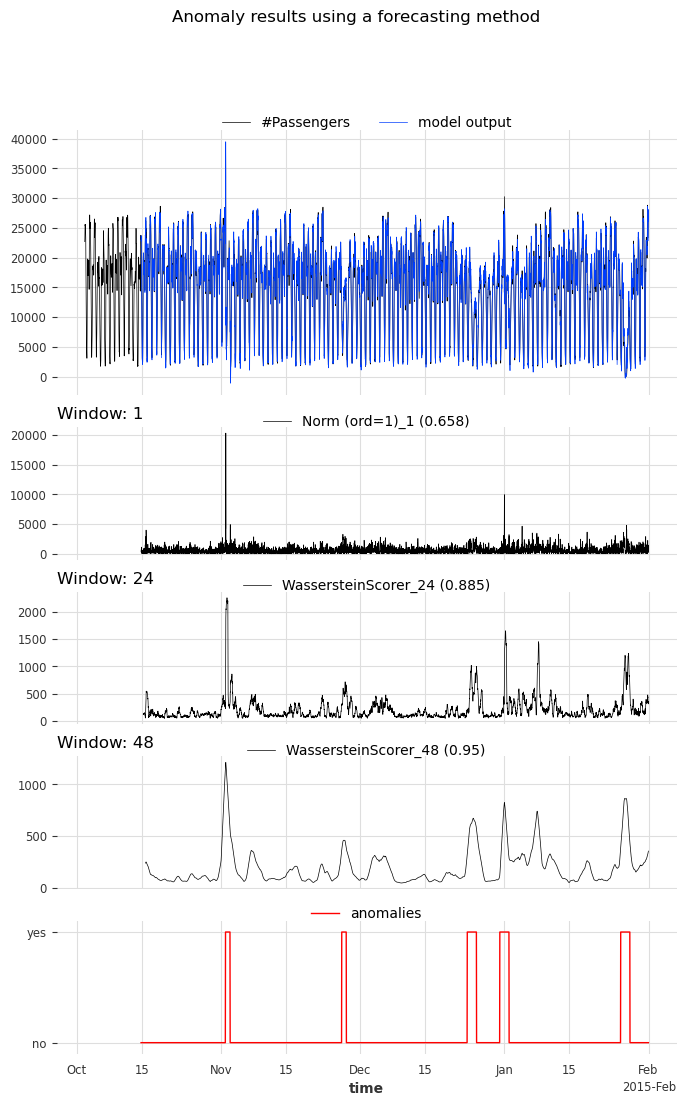

show_anomalies_from_scores(

series=s_taxi_test,

anomalies=series_taxi_anomalies[pred_start:],

pred_scores=anomaly_scores,

pred_series=model_forecasting,

window=windows,

title="Anomaly results using a forecasting method",

names_of_scorers=scorer_names,

metric="AUC_ROC",

)

A zoom on each anomalies: visualize the results#

[18]:

def plot_anom_eval(selected_anomaly, delta_plotted_days):

one_day = series_taxi.freq * 24 * 2

anomaly_date = anomalies_day[selected_anomaly][0]

start = anomaly_date - one_day * delta_plotted_days

end = anomaly_date + one_day * (delta_plotted_days + 1)

# input series and forecasts

series_taxi[start:end].plot(

label="Number of taxi passengers", color="#6464ff", linewidth=0.8

)

model_forecasting[start:end].plot(

label="Model prediction", color="green", linewidth=0.8

)

# actual anomalies and predicted scores

(series_taxi_anomalies[start:end] * 10000).plot(

label="Known anomaly", color="r", linewidth=0.8

)

# Scaler transforms scores into a value range between (0, 1)

(Scaler().fit_transform(best_anomaly_score)[start:end] * 10000).plot(

label="Anomaly score", color="black", linewidth=0.8

)

plt.legend(loc="upper center", ncols=2)

plt.title(selected_anomaly)

fig.tight_layout()

plt.show()

for anom_name in anomalies_day:

plot_anom_eval(anom_name, 3)

break # remove this to see all anomalies

Simple case: KMeansScorer#

Let’s have a closer look at the scorer’s window parameter on the example of the KmeansScorer. We’ll use two toy datasets to demonstrate how the scorers perform with different window sizes. In first example we set window=1 on a multivariate time series, and in the second we set window=2 on a univariate time series.

The figure below illustrates the Scorer’s windowing process:

Multivariate case with window=1#

Synthetic data creation#

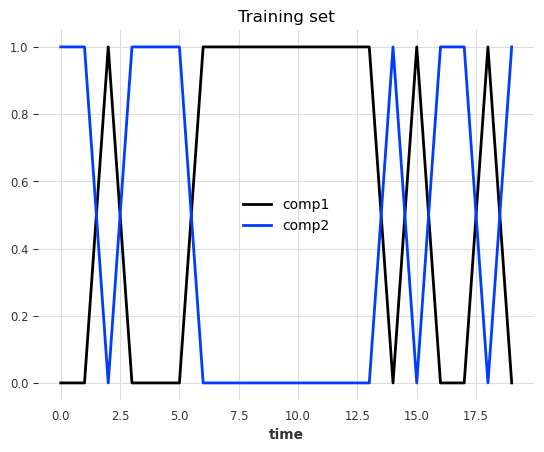

The data is a multivariate series (2 components/columns). Each step has either value of 0 or 1, and the two components always have opposite values:

[19]:

pd.DataFrame(index=["State 1", "State 2"], data={"comp1": [0, 1], "comp2": [1, 0]})

[19]:

| comp1 | comp2 | |

|---|---|---|

| State 1 | 0 | 1 |

| State 2 | 1 | 0 |

At each timestamp, it has a 50% chance to switch state and a 50% chance to keep the same state.

Train set#

[20]:

def generate_data_ex1(random_state: int):

np.random.seed(random_state)

# create the train set

comp1 = np.expand_dims(np.random.choice(a=[0, 1], size=100, p=[0.5, 0.5]), axis=1)

comp2 = (comp1 == 0).astype(float)

vals = np.concatenate([comp1, comp2], axis=1)

return vals

[21]:

data = generate_data_ex1(random_state=40)

series_train = TimeSeries.from_values(data, columns=["comp1", "comp2"])

# visualize the train set

series_train[:20].plot()

plt.title("Training set")

plt.show()

Test set#

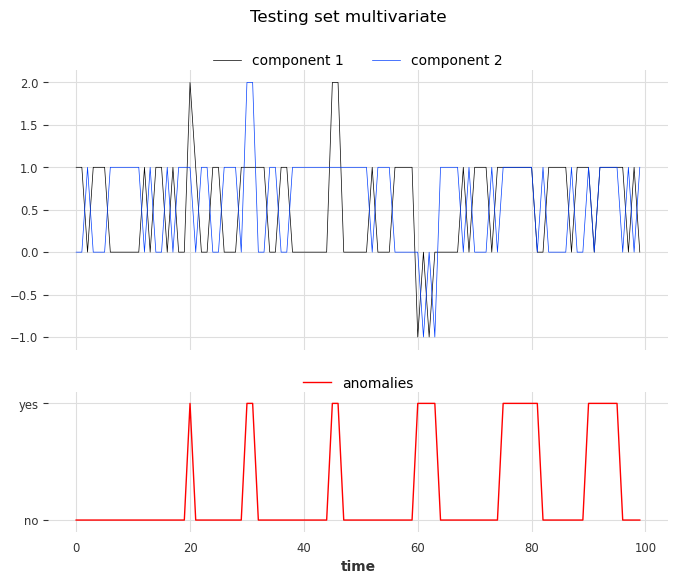

We create the test set using the same rules as the train set but we’ll inject six anomalies of three different types. The anomalies can be longer than one timestamp. The types are:

1st type: replacing the value of one component (0 or 1) with 2

2nd type: adding +1 or -1 to both components

3rd type: both components have the same value

[22]:

# inject anomalies in the test timeseries

data = generate_data_ex1(random_state=3)

# 2 anomalies per type

# type 1: random values for only one component

data[20:21, 0] = 2

data[30:32, 1] = 2

# type 2: shift both components values (+/- 1 for both components)

data[45:47, :] += 1

data[60:64, :] -= 1

# type 3: switch one value to the another

data[75:82, 0] = data[75:82, 1]

data[90:96, 1] = data[90:96, 0]

series_test = TimeSeries.from_values(data, columns=["component 1", "component 2"])

# create the binary anomalies ground truth series

anomalies = ~((data == [0, 1]).all(axis=1) | (data == [1, 0]).all(axis=1))

anomalies = TimeSeries.from_times_and_values(

times=series_test.time_index, values=anomalies, columns=["is_anomaly"]

)

Let’s look at the anomalies. From left to right, the first two anomalies correspond to the first type, the third and the fourth correspond to the second type, and the last two to the third type.

[23]:

show_anomalies_from_scores(

series=series_test, anomalies=anomalies, title="Testing set multivariate"

)

Use the scorer KMeansScorer()#

We’ll use the KMeansScorer to locate the anomalies with the following parameters:

k=2: The number of clusters/centroids generated by the KMeans model. We choose two since we know that there are only two valid states.window=1 (default): Each timestamp is considered independently by the KMeans model. It indicates the size of the window used to create the subsequences of the series (windowis identical to a positive targetlagfor our regression models). In this example we know that each anomaly can be detected by only looking one step.component_wise=False (default): All components are used together as features with a single KMeans model. IfTrue, we would fit a dedicated model per component. For this example we need information about both components to find all anomalies.

We’ll fit KMeansScorer on the anomaly-free training series, compute the anomaly scores on the test series, and finally evaluate the scores.

[24]:

Kmeans_scorer = KMeansScorer(k=2, window=1, component_wise=False)

# fit the KmeansScorer on the train timeseries 'series_train'

Kmeans_scorer.fit(series_train)

[24]:

<darts.ad.scorers.kmeans_scorer.KMeansScorer at 0x29a3849d0>

[25]:

anomaly_score = Kmeans_scorer.score(series_test)

# visualize the anomaly score compared to the true anomalies

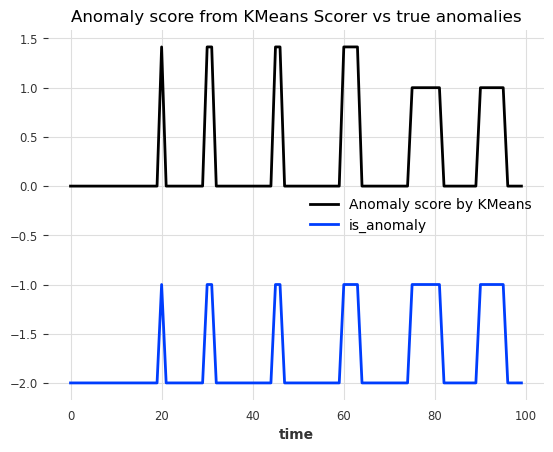

anomaly_score.plot(label="Anomaly score by KMeans")

(anomalies - 2).plot()

plt.title("Anomaly score from KMeans Scorer vs true anomalies")

plt.show()

Nice! We can see that the anomaly scores accurately indicate the position of the 6 anomalies.

To evaluate the scores, we can call eval_metric(). It expects the true anomalies, the series, and the name of the agnostic threshold metric (AUC-ROC or AUC-PR).

[26]:

for metric_name in ["AUC_ROC", "AUC_PR"]:

metric_val = Kmeans_scorer.eval_metric(anomalies, series_test, metric=metric_name)

print(metric_name + f": {metric_val}")

AUC_ROC: 1.0

AUC_PR: 1.0

And again, let’s visualize the results with show_anomalies():

[27]:

Kmeans_scorer.show_anomalies(series=series_test, anomalies=anomalies, metric="AUC_ROC")

Univariate case with window>1#

In the previous example, we used window=1 which was sufficient to identify all anomalies. In the next example, we’ll see that sometimes higher values are required to capture the true anomalies.

Synthetic data creation#

Train set#

In this toy example, we generate a univariate (one component) series that can take 4 possible values.

possible values at each step

(0, 1, 2, 3)every next step either adds

diff=+1or subtractsdiff=-1(50% chance)all steps are upper- and lower-bounded

0anddiff=-1remains at03anddiff=+1remains at3

[28]:

def generate_data_ex2(start_val: int, random_state: int):

np.random.seed(random_state)

# create the test set

vals = np.zeros(100)

vals[0] = start_val

diffs = np.random.choice(a=[-1, 1], p=[0.5, 0.5], size=len(vals) - 1)

for i in range(1, len(vals)):

vals[i] = vals[i - 1] + diffs[i - 1]

if vals[i] > 3:

vals[i] = 3

elif vals[i] < 0:

vals[i] = 0

return vals

[29]:

data = generate_data_ex2(start_val=2, random_state=1)

series_train = TimeSeries.from_values(data, columns=["series"])

# visualize the train set

series_train[:40].plot()

plt.title("Training set")

[29]:

Text(0.5, 1.0, 'Training set')

Test set#

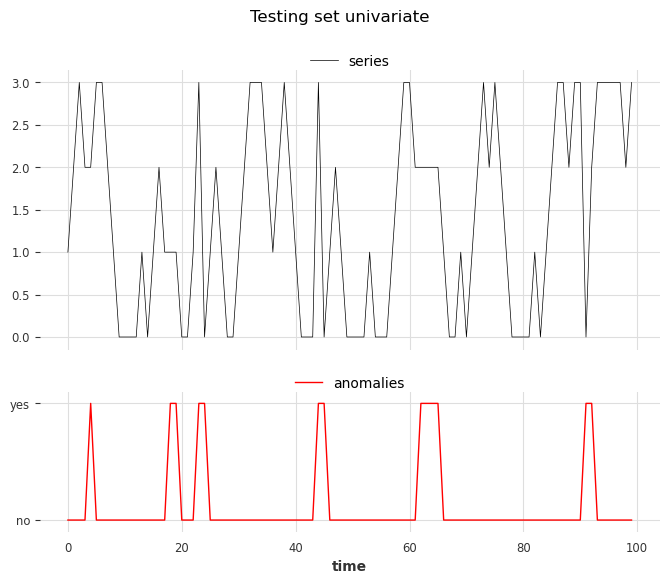

We create the test set using the same rules as the train set but we’ll inject six anomalies of two different types. The anomalies can be longer than one timestamp:

Type 1: steps with

abs(diff) > 1(jumps larger than one)Type 2: steps with

diff = 0at values(1, 2)(value remains constant)

[30]:

data = generate_data_ex2(start_val=1, random_state=3)

# 3 anomalies per type

# type 1: sudden shift between state 0 to state 2 without passing by value 1

data[23] = 3

data[44] = 3

data[91] = 0

# type 2: having consecutive timestamps at value 1 or 2

data[3:5] = 2

data[17:19] = 1

data[62:65] = 2

series_test = TimeSeries.from_values(data, columns=["series"])

# identify the anomalies

diffs = np.abs(data[1:] - data[:-1])

anomalies = ~((diffs == 1) | ((diffs == 0) & np.isin(data[1:], [0, 3])))

# the first step is not an anomaly

anomalies = np.concatenate([[False], anomalies]).astype(int)

anomalies = TimeSeries.from_times_and_values(

series_test.time_index, anomalies, columns=["is_anomaly"]

)

[31]:

show_anomalies_from_scores(

series=series_test, anomalies=anomalies, title="Testing set univariate"

)

plt.show()

From left to right, anomalies at positions 3, 4, and 6 are of type 1, and anomalies at positions 1, 2, and 5 are of type 2.

Use the scorer KMeansScorer()#

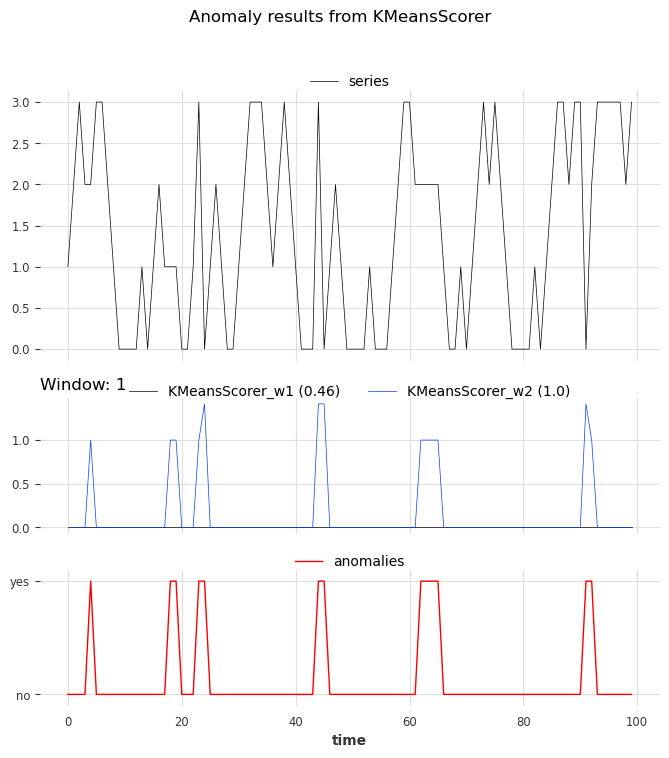

We fit two KMeansScorer with different values for the window parameter (1 and 2).

[32]:

windows = [1, 2]

Kmeans_scorer_w1 = KMeansScorer(k=4, window=windows[0])

Kmeans_scorer_w2 = KMeansScorer(k=8, window=windows[1], window_agg=False)

[33]:

scores_all = []

metric_data = {"AUC_ROC": [], "AUC_PR": []}

for model, window in zip([Kmeans_scorer_w1, Kmeans_scorer_w2], windows):

model.fit(series_train)

scores = model.score(series_test)

scores_all.append(scores)

for metric_name in metric_data:

metric_data[metric_name].append(

eval_metric_from_scores(

anomalies=anomalies,

pred_scores=scores,

metric=metric_name,

)

)

pd.DataFrame(data=metric_data, index=["w_1", "w_2"])

[33]:

| AUC_ROC | AUC_PR | |

|---|---|---|

| w_1 | 0.460212 | 0.123077 |

| w_2 | 1.000000 | 1.000000 |

The metric indicates that the scorer with the parameter window set to 1 cannot locate the anomalies. On the other hand, the scorer with the parameter set to 2 perfectly identified the anomalies.

[34]:

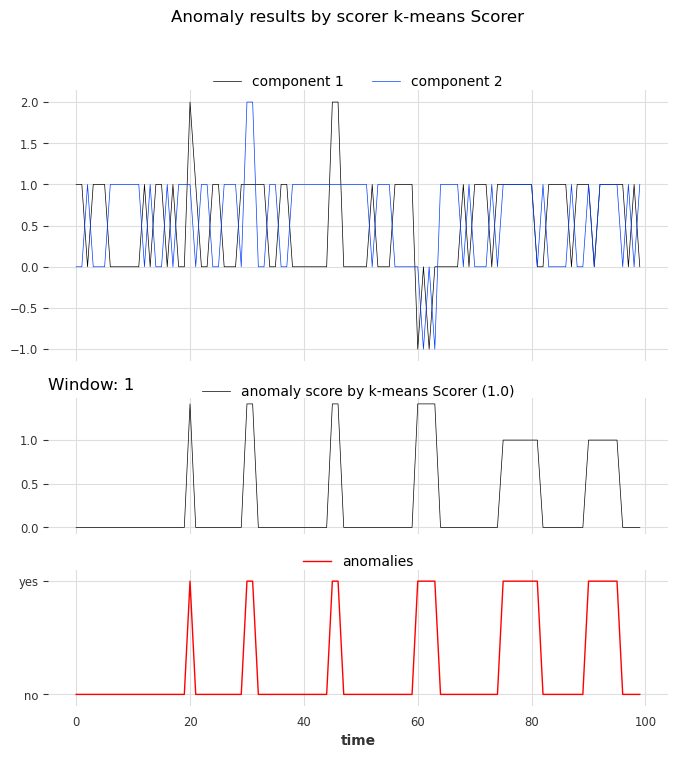

show_anomalies_from_scores(

series=series_test,

anomalies=anomalies,

pred_scores=scores_all,

names_of_scorers=["KMeansScorer_w1", "KMeansScorer_w2"],

metric="AUC_ROC",

title="Anomaly results from KMeansScorer",

)

We can see the accurate prediction of the scorer with a window of 2 compared to that of the scorer with a window of 1.

[ ]: